In the stock market Momentum denotes the rate of change in the price of a stock.

A stock that is in trend demonstrates price persistence and a tendency to continue to move in its present direction. Momentum investing seeks to exploit this phenomenon in the markets.

Academic Validation

Jagdeesh and Titman’s 1993 paper called Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency

This paper documents that strategies that buy stocks that have performed well in the past and sell stocks that have performed poorly in the past generate significant positive returns. The profitability of these strategies is not due to their systematic risk or to delayed stock price reactions to common factors.

Eugene Fama and Kenneth French 2008 called “Dissecting Anomalies”

The anomalous returns associated with net stock issues, accruals, and momentum are pervasive; they show up in all size groups (micro, small, and big) in cross-section regressions, and they are also strong in sorts, at least in the extremes.

Tobias West 2022 called Momentum: What do we know 30 years after Jagdeesh and Titman’s seminal paper

For over 30 years, extensive research has found corroborating evidence that past winners continue to yield higher returns than past losers. This momentum effect is robust across various asset classes and across the globe and presents perhaps the most pervasive contradiction of the efficient market hypothesis.

Factor Returns

Factor returns emanate from factor investing.

Factor investing is an approach that focuses on specific drivers of returns across asset classes. The more popular among factor investing involves focusing on investment style.

Numerous factors have been discovered, but only a handful of them have won general approval from the academic community and show robust empirical results through time :

- Size – Excess returns of smaller counterparts relative to their larger peers

- Value – Excess returns of stocks that have low prices relative to their fundamental value

- Quality- Excess returns from stocks that have quality metrics like low debt, stable earnings growth

- Low Volatility- Excess returns from stocks with lower than average volatility/beta

- Momentum – Excess returns of stocks with stronger past performance.

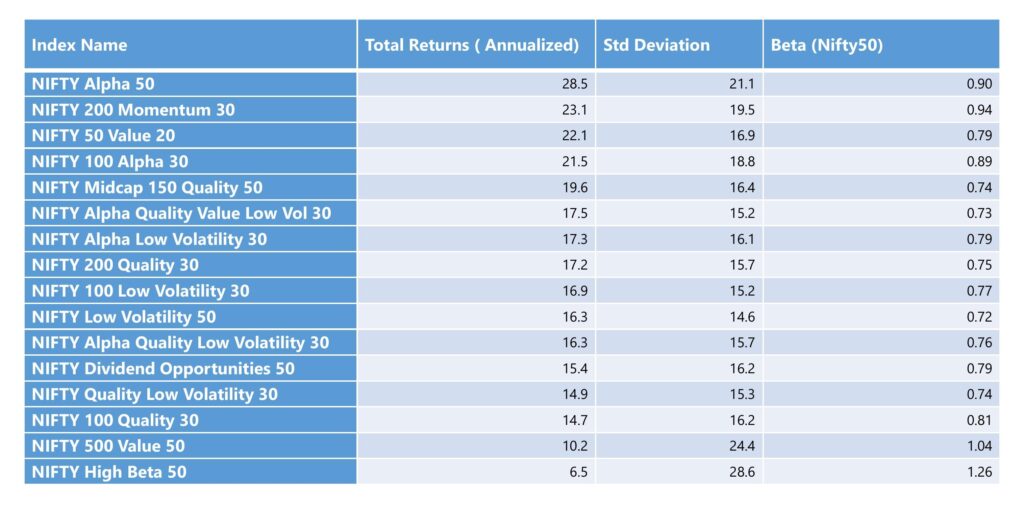

Factor Returns – Factor Indices v Nifty 50 (3-year trailing return)

Factor Returns – Factor Indices v Nifty 50 (3 year trailing return)

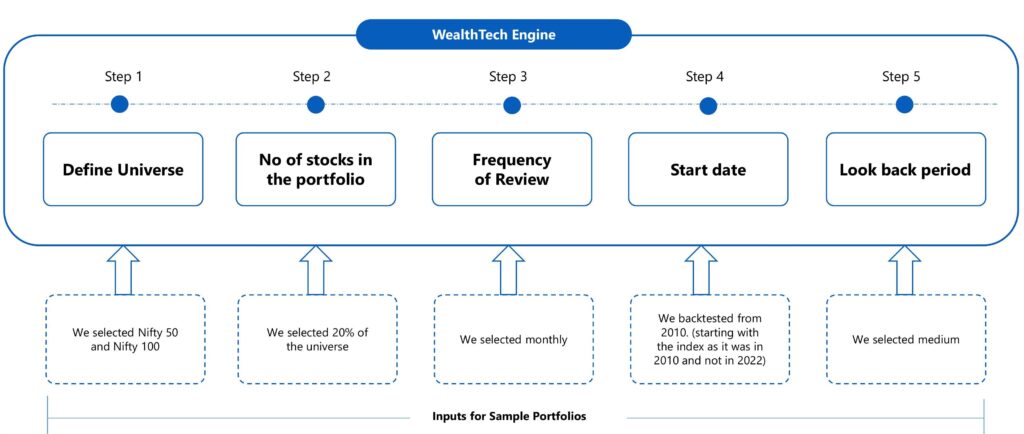

Creating portfolios using Smartvalues WealthTech Engine

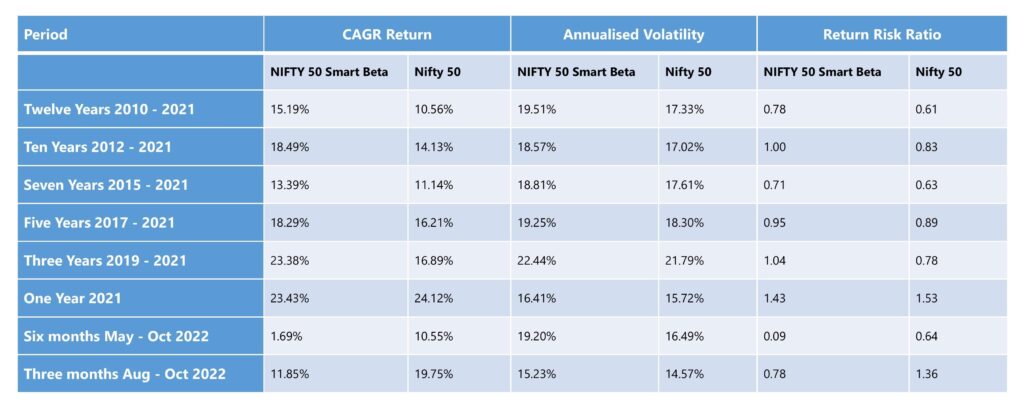

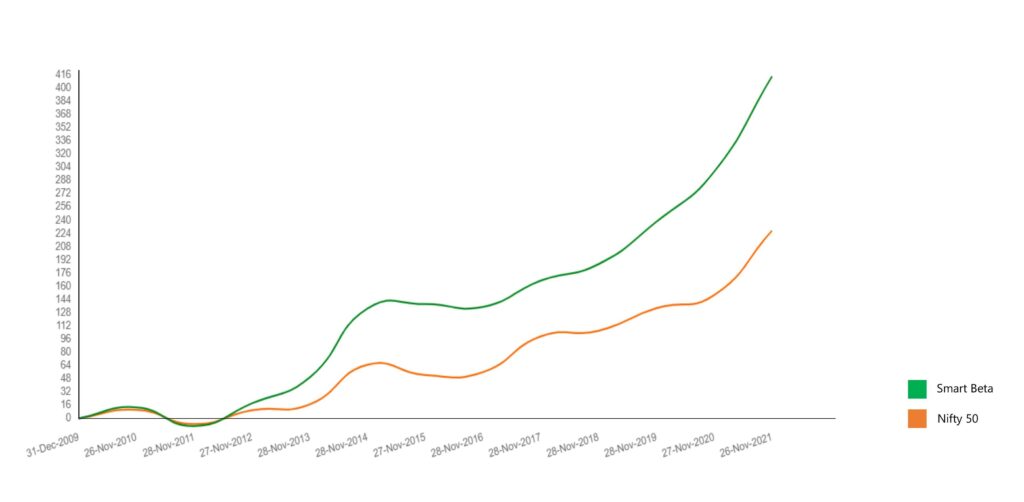

Our Sample Portfolio – Nifty 50 Smart Beta

Though Nifty 50 Smart Beta has a higher volatility it has maintained a higher risk adjusted ratio.

Nifty 50 Smart Beta

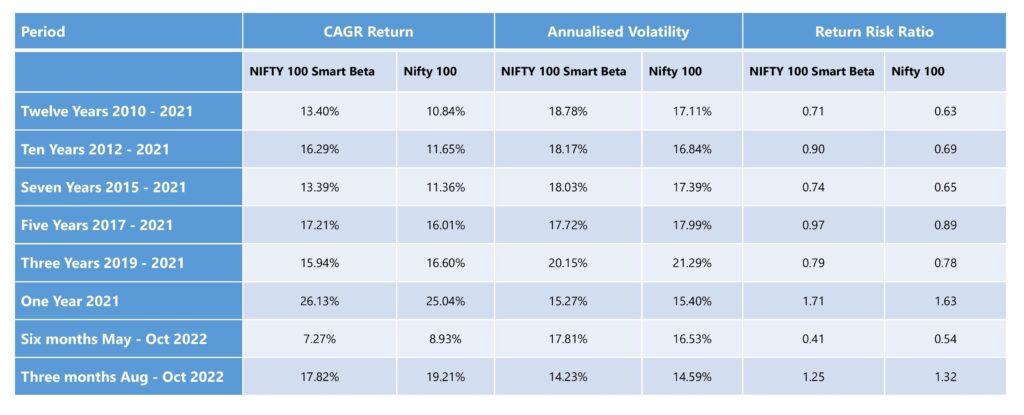

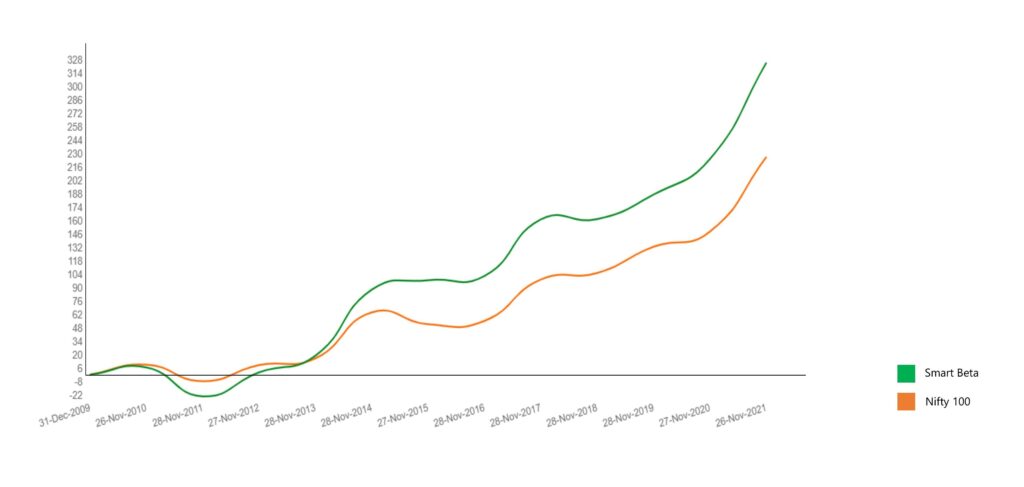

Our Sample Portfolio – Nifty 100 Smart Beta

Nifty 100 Smart Beta

Conclusion

- Factors have been identified as key constituents of risk and returns.

- Momentum is a factor that usually features at the top of the ladder.

- Smartvalues is a convenient way of creating Smartbeta and other portfolios using the momentum factor.

- Generates superior risk-adjusted returns.